Get the latest insights on India’s tech sector slowdown, Maharashtra’s GCC city plans,

Anthropic’s expansion into India and more. Tune in to this episode of The GCC Hub Podcast

to stay ahead of the curve in the world of Global Capability Centres.

Tag: GCC India

-

Episode 27: GCCs Shine Amidst Tech Slowdown & Maharashtra’s GCC City Plans

-

India’s Global Capability Centres Set to Reach 5,000; ICAI Hosts Inaugural Summit

India is poised to become home to 5,000 global capability centres (GCCs) in the next two years, driven by the country’s robust digital systems, stable regulatory frameworks, and skilled workforce. The Institute of Chartered Accountants of India (ICAI) recently hosted its first-ever GCC Summit 2025 in Delhi, bringing together over 500 leaders from the GCC, finance, and technology sectors.

The summit, themed ‘From Ledgers to Global Leadership,’ aims to foster dialogue, innovation, and actionable insights to drive the growth of India’s GCC sector. According to Mahaveer Singhvi, Joint Secretary, Ministry of External Affairs, Indian chartered accountants are seen as “custodians of trust” in the evolving business ecosystem.

Key highlights of India’s GCC sector include the fact that India currently accounts for more than 50% of all GCCs being set up globally, with over 1,700 GCCs already operational and serving more than 1,000 global corporations, employing around 2 million professionals in India, with this number expected to increase significantly in the coming years. GCCs are also expected to bring in over US$100 billion in export earnings by 2030. To support the growth of the GCC sector, ICAI has introduced certification courses tailored to global markets and created a system to train and place chartered accountants in GCCs.

The ICAI plans to conduct similar summits in Ahmedabad, Mumbai, and Hyderabad in the coming months, providing chartered accountants with opportunities to learn from industry leaders and gain insights into future trends. The institute aims to attract fresh talent and address gaps in the profession through these initiatives ².

India’s emergence as a hub for GCCs is driven by its rigorous training ecosystem, abundant talent pool, and government support. With the number of GCCs expected to surpass 5,000 in the next two years, India is set to become an even more prominent player in the global business services industry.

-

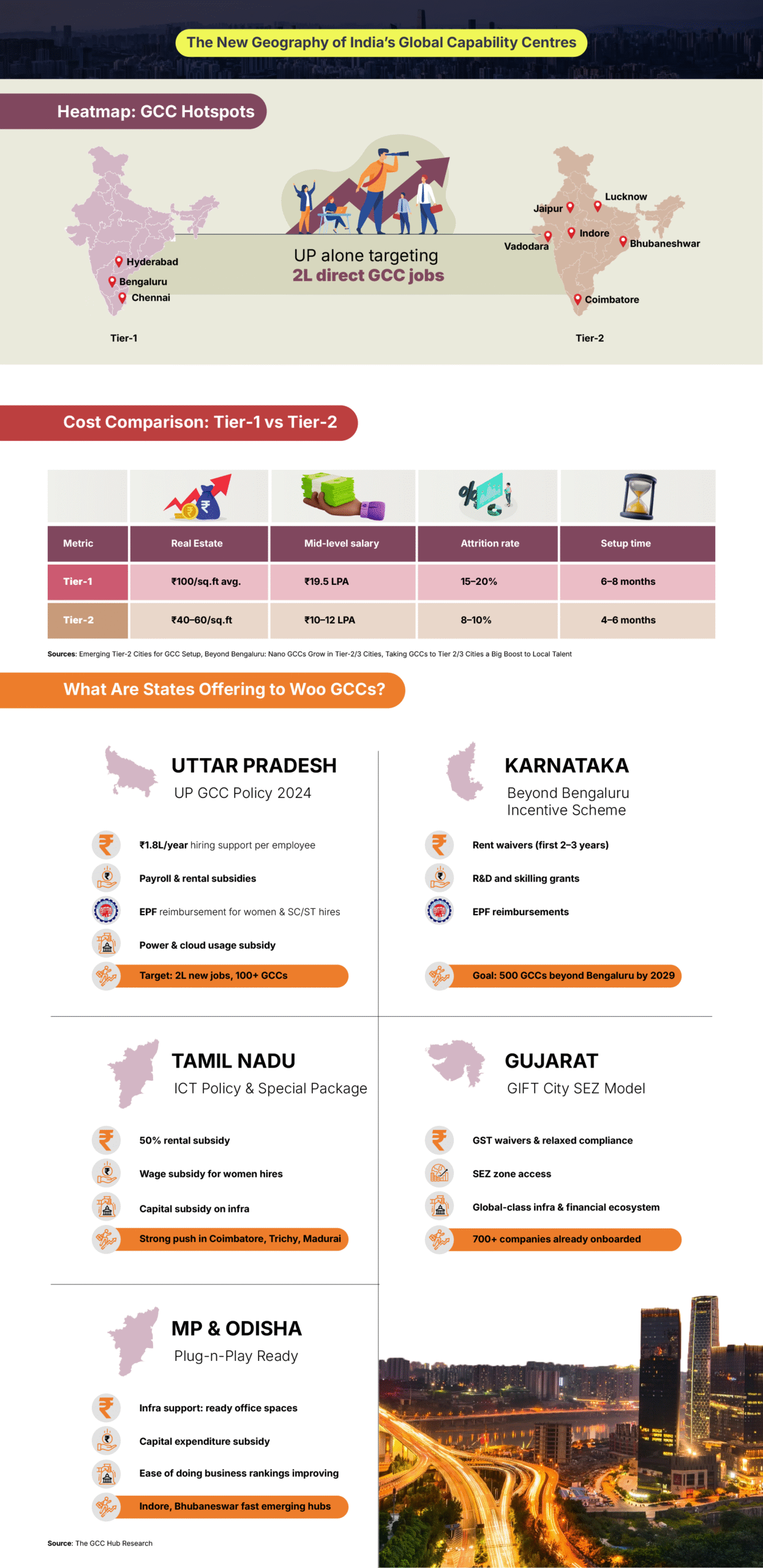

The New Geography of India’s Global Capability Centres

India’s GCC story is at an inflection point, with smaller cities in states like Uttar Pradesh, Tamil Nadu, Gujarat, and Karnataka positioning themselves as the next major hubs for Global Capability Centres. According to data, GCC presence in tier-2 and tier-3 locations is expected to grow by 15–20% by 2025. For the states, it’s game on.

-

GCC Exports Reveal Faster Relative GrowthKey Metrics for Infographic

On the revenue front, India’s IT sector clocked $254 billion in 2024, while GCCs generated $65 billion, showing faster relative growth. GCCs are no longer mere support hubs but strategic centers driving global innovation. Their increasing market cap and job additions signal a shift toward high-margin, product-driven capabilities rather than traditional IT outsourcing. This transformation reflects India’s evolving position as a global digital economy leader, with policy incentives and a skilled talent pool attracting greater GCC investments. If the trend continues, GCCs could rival IT services in total employment and revenue by the next decade, reshaping India’s macroeconomic and employment landscape.

Source: Nasscom, Zinnov, Quess, Moneycontrol Research

https://www.moneycontrol.com/technology/gccs-outpace-it-in-2024-way-ahead-in-job-addition-market-cap-article-12901002.html -

How India’s Global Capability Centres are Redefining the IT-Services Landscape

The traditional outsourcing model that built India’s IT services empire is facing its most significant challenge in decades. Global Capability Centers (GCCs) have evolved from back-office cost centers to strategic innovation hubs, reshaping the competitive dynamics for established players like Tata Consultancy Services (TCS), Infosys, and Wipro.

The timing of this transformation becomes particularly relevant given the recent emphasis at TCS’s Annual General Meeting (AGM), where independent director Keki Mistry highlighted the imperative to “proactively explore collaboration with GCCs” and noted that “TCS’s clients continue to derive substantial value from their partnership with the company, which is exploring engagement models to collaborate with GCCs”. Recently, at Infosys’ 44th AGM, chairman and co-founder Nandan Nilekani echoed a similar sentiment, highlighting that GCCs are now critical clients rather than competitors. He emphasised that the current wave of GCCs is driven by innovation arbitrage rather than cost arbitrage.

The numbers tell a compelling story of transformation. India currently hosts approximately 1,800 GCCs employing over 2.1 million professionals, with the total market size having reached US$72-76 billion in early 2025. The most striking indicator of this transformation is the emergence of billion-dollar GCC powerhouses. About 24 GCCs crossed the US$1 billion export revenue milestone in FY 2023-24, up from just 12 five years earlier, collectively generating exports exceeding US$43.6 billion. GCCs are projected to create 4.25-4.5 lakh new jobs in 2025 alone, with the sector aiming for a 50% workforce increase by 2030. Perhaps most significantly for IT-services firms, 70% of Fortune 500 companies are expected to expand their presence in India by 2030, with over 500 centres now dedicated to AI and machine learning.

What makes the GCC revolution particularly disruptive is its fundamental departure from the traditional outsourcing model. While conventional IT services rely on third-party relationships, GCCs represent a strategic insourcing trend where multinational corporations are bringing critical functions in-house. Over 70% of GCCs in India are now actively driving digital transformation initiatives for their parent organisations, moving far beyond the cost-arbitrage model that originally defined the sector. The shift is particularly pronounced in high-value functions, with GCCs increasingly taking ownership of AI development, digital transformation, R&D activities, and product development areas that were traditionally the bread and butter of IT services companies.

The Economic Reality of Transformation

Recognising the challenge, India’s IT majors are pivoting from viewing GCCs as competitors to embracing them as collaboration partners. This strategic shift is already yielding tangible results. Infosys’s India revenue grew 19.9% and 16% sequentially in the first and second quarters of fiscal 2025, whilst TCS saw a remarkable 95.2% expansion in revenue from the home market, which now accounts for 5.6% of total revenue.

However, despite signs of collaboration-driven success, the traditional IT services model is under pressure. Top-tier IT firms are dealing with sluggish growth, cautious forecasts, and cost-cutting measures—highlighting ongoing structural challenges in the sector.

The collaboration with GCCs takes multiple forms across the industry, but it comes at a cost. Infosys CEO and MD Salil Parekh outlined the company’s comprehensive GCC engagement strategy, describing how they work with GCCs during Build-Operate-Transfer transitions, help scale operations, assist with recruiting, and even work with clients when they exit GCC arrangements. This approach was demonstrated when Infosys acquired Danske Bank’s GCC business in September, which had been operating in India for 10-15 years. Yet industry executives acknowledge that GCC business “is a little less profitable because sometimes the contracts are in rupees… the US business is usually more profitable”.

The scale of the transformation is evident in the geographic distribution of GCCs. As of December 2024, there are over 1,950 GCC units in the country, accounting for more than one-third of the occupied office space in India’s top seven markets. Perhaps the most immediate challenge facing IT-services companies is the intensifying war for talent. GCCs remain top employers, thanks to their competitive compensation—often paying a 30% premium over IT companies—at a time when traditional firms are seeing a slowdown in workforce growth. The competition is particularly fierce in emerging technologies, with GCCs now employing over 120,000 AI professionals across centers of excellence in India, creating a significant talent pool that might otherwise have been available to traditional IT players.

Collaboration Over Competition

Today, GCCs are driving AI-powered research and development initiatives, building new products and solutions whilst ensuring continuous innovation. This represents a fundamental shift from the traditional IT-services model, where innovation was often secondary to execution efficiency. The convergence of GCCs with Generative AI is creating new possibilities for rapid prototyping, predictive analytics, and automation that enhance agility and responsiveness.

Despite initial concerns about revenue cannibalisation, industry leaders are increasingly viewing the GCC phenomenon as complementary rather than competitive. As ANSR co-founder Vikram Ahuja observed, there is a common misconception that GCCs and service providers compete with each other, when in reality, 85% of GCC customers also work with IT-services companies in some capacity. The emerging consensus suggests a hybrid ecosystem where GCCs will spearhead innovation, take charge of customer relationships, and lead product development, whilst IT service firms provide operational strength, cross-domain knowledge, and delivery capabilities.

For TCS, Infosys, Wipro, and other IT-services majors, this creates both unprecedented challenges and significant opportunities. The companies that successfully navigate this transition will be those that embrace collaboration over competition, invest in specialised capabilities over standardised services, and focus on value creation over cost reduction.

The future belongs to those who can orchestrate this new ecosystem, where the lines between insourcing and outsourcing are blurring, and success hinges on integrating the innovation capacity of GCCs with the execution strength of established IT-service providers. The GCC revolution represents more than a shift in outsourcing preferences – it signals a fundamental transformation in how global enterprises structure their technology and innovation capabilities.

-

Global Capability Centres Now Critical Clients: Infosys Chairman Nandan Nilekani

Infosys Chairman and Co-founder Nandan Nilekani said on June 25 that global capability centres (GCCs) have become critical clients for the IT-services giant, rather than competitors. Addressing shareholders at the company’s 44th Annual General Meeting, Nilekani emphasised that the current wave of GCCs is focused on innovation arbitrage, rather than cost arbitrage.

GCCs, captive units set up by companies to carry out IT and related business functions, have become a significant part of India’s economy. India is home to almost 1,700 GCCs, employing close to 2 million people, and is expected to contribute 3.5% to the country’s GDP by 2030.

Nilekani said Infosys is actively supporting GCCs in developing advanced technological capabilities, particularly in emerging areas like artificial intelligence (AI) and machine learning (ML). “Quite a few companies are setting up research centers, AI-ML centers in GCCs, and we’re helping many of them in this regard,” he added.

The company has made significant strides in AI adoption, with over 20,000 employees actively using GitHub for coding. Salil Parekh, CEO and MD, Infosys, said the company is among the largest users of the platform in the IT industry. The company has generated 10 million lines of code and developed four proprietary small language models tailored for key sectors, including financial services, IT operations, and cybersecurity.

Nilekani also highlighted the changing global economic landscape, describing the current macroeconomic environment as a “perfect storm” where traditional globalisation models are rapidly disintegrating. “The world is moving from a single global market to fragmented blocks,” he said, adding that businesses must develop region-specific strategies, diversify supply chains, and adapt to varying regulatory environments to stay competitive.

-

How Indian GCCs Are Emerging as Frontline Architects of Global ESG

As Europe tightens ESG disclosure rules and the U.S. dials down its climate rhetoric, India’s Global Capability Centres (GCCs) find themselves in the eye of a regulatory storm. These 1,500-plus operational hubs for Fortune 500 firms are now making high-stakes decisions on carbon targets, compliance frameworks, and brand integrity, effectively becoming ESG architects for their parent companies.

According to EY, GCCs are evolving into ESG Centres of Excellence, going beyond compliance to drive global sustainability agendas. With over 1.66 million professionals, they manage everything from emissions tracking to supply chain risk, positioning India as a nerve centre of corporate climate action.

India’s ESG framework has become increasingly codified. According to India Briefing, it began with voluntary CSR guidelines in 2009, culminating in the mandatory CSR clause of the Companies Act, 2013. SEBI’s Business Responsibility and Sustainability Reporting (BRSR) norms, rolled out in 2021, made ESG reporting compulsory for India’s top 1,000 listed firms. Taxmann notes that BRSR Core, a stricter framework with 42 KPIs, became mandatory for the top 150 companies from FY 2023-24.

While environmental regulation is backed by legacy laws like the Environment Protection Act (1986), governance is anchored by statutes such as the Prevention of Corruption Act (1988) and the Money Laundering Act (2002).

The EU Tightens, the U.S. Rebrands

According to India Briefing, the EU’s Corporate Sustainability Reporting Directive (CSRD) demands granular disclosures on emissions and human rights. The Carbon Border Adjustment Mechanism (CBAM) adds economic weight, applying tariffs on carbon-intensive imports.

Meanwhile, the Trump administration’s return in 2025 has prompted a semantic pivot. According to Bloomberg, U.S. companies are dropping the term “ESG” in response to political backlash. However, Reuters notes that most continue to pursue the same targets under different labels, pushed by investors and global compliance.

This duality – stringent in Europe, symbolic in the U.S. – requires Indian GCCs to decode and align competing frameworks while maintaining operational coherence.

Playbook in Action: Centralised, Data-Driven, Adaptive

According to EY, many GCCs now run centralised ESG units that integrate global reporting frameworks like Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SASB) with India’s BRSR. This consolidation ensures consistent data flows and audit trails.

Real-time metrics are another key lever. According to Inductus GCC, AI and analytics platforms, like the carbon accounting tool from IIM Bangalore, help track Scope 1, 2, and 3 emissions, aligning local and international compliance.

Supply chains are being overhauled, too. With 72% of Gen Z and 77% of millennials demanding sustainable products, GCCs are embedding ESG into procurement, logistics, and waste reduction.

Mind the Gap: Ambition vs. Reality

India’s climate goals are bold, net zero by 2070 and a 45% drop in carbon intensity by 2030. The interim goals include 500 GW of non-fossil energy and 50% renewable power integration.

But the terrain is bumpy. EY flags skill gaps in ESG functions, while also highlighting the dissonance between BRSR and global standards. Inductus GCC points to opaque supply chains as a roadblock, especially for smaller GCCs that also face bandwidth and funding constraints.

Still, EY India’s ESG GCC Survey 2024 reports that as of April 2024, 67% of GCCs are drafting sustainability strategies, 52% have “proactively” adopted ESG policies and are refining processes to anchor them and 70% are turning to tech partnerships. Materiality assessments and SMART goals are helping focus efforts.

Trump Card: Same Goals, New Language

The Trump administration’s deregulatory stance has triggered linguistic gymnastics in the U.S. ESG landscape. According to Bloomberg, terms like “resilience” and “risk mitigation” are replacing “ESG” to avoid political heat. But as Reuters notes, the targets remain.

For Indian GCCs, especially those serving U.S. clients, this means adapting the language while preserving the outcomes. According to Sweep, many now rely on science-based frameworks like Science Based Targets initiative (SBTi) to track emissions, avoiding ESG branding but delivering ESG impact.

According to PwC, enterprise software used by GCCs is being retooled with sustainability analytics, integrating ESG into everyday operations. What began as compliance reporting is now a strategic asset, boosting efficiency, managing risk, and reinforcing global competitiveness.

This linguistic sleight-of-hand hasn’t dulled the intensity of the mission. GCCs are doubling down on measurable outcomes, from cutting emissions to greening data centres and embedding sustainability into tech stacks.

India’s ESG framework may still be catching up with global peers in terms of rigour. But its GCCs are sprinting ahead—turning regulatory complexity into business advantage, and emerging not just as executors, but as ESG architects for the world.

In a world of shifting policies and polarised narratives, the one constant is accountability. And increasingly, the map to global ESG compliance runs straight through India’s GCC corridors.

-

Episode 12: India’s GCC Landscape: Growth, Innovation, and Opportunity

In this episode, we dive into the latest developments shaping India’s Global Capability Centre (GCC) landscape. Discover how India-based GCCs are evolving into global hubs for complex tax operations and innovation. From major new GCC launches to the shift from service delivery to strategic innovation–and its impact on the IT sector–we cover it all.

Key Topics:

– India-based GCCs and complex tax operations

– Toyo and MODEC’s new GCC in Bengaluru

– GCCs evolve from delivery centers to innovation hubs

– GCCs drive tech hiring despite muted IT sector growth

– Ferguson’s new GCC powered by ANSR in Bengaluru

To stay informed about the world of GCCs, tune in now!

-

Flexibility, Well-Being, Work-Life Balance: GCCs’ Hook to Lure Talent

Today, job seekers want more than just a high-paying job. They are looking for work flexibility, meaningful roles, mentorship, autonomy and a positive company culture. To meet these evolving expectations, Global Capability Centres (GCCs) in the country are increasingly offering benefits such as comprehensive healthcare, including mental health support, elder care and on-site childcare. These policies go beyond the flexibility of remote work, helping not only to retain talent but also to boost productivity.

Take Bengaluru-based Anisha Singh, a young mother and software engineer at a GCC, who considers the on-site childcare facility provided by her employer as the most valuable perk.

“Knowing that my two-year-old is just 500 metres from my desk puts me at peace,” she says. “I can get to him quickly if there’s an emergency and, surprisingly, it’s made me more productive.”

New mothers make up the largest share of those who step away from their careers. These breaks often lead to employment gaps and added challenges when returning to work. In response, GCCs are working to ensure they don’t lose skilled talent in the process.

The Covid-19 pandemic accelerated a global shift in how we work, and India’s GCCs have been quick to adapt to the changing needs. From remote and hybrid work models to flexible hours and location-independent hiring, they are leading the charge in offering work-life balance. These policies are especially crucial in attracting talent from Tier-2 and Tier-3 cities, expanding the talent pool while supporting decentralisation.

They are offering Employee Assistance Programmes (EAPs) focused on the holistic well-being of the employees with perks like gym subsidies, subscription to wellness apps, insurance with mental health coverage and others. Multigenerational workforce have diverse needs, and while tech giants and multinationals have been offering customised perks and benefits, GCCs are not far behind. Inclusive workplace policies reflect the larger purpose of the organisation, of being empathetic. For instance, mushrooming of GCCs across tier-2 and tier-3 cities has created more women representation in the workforce, as many could take up their jobs without leaving their hometowns.

Talent retention is another challenge that GCCs are addressing by offering a well-defined career planning process including targeted learning opportunities such as upskilling and training to keep pace with the changing job market. Working with teams across geographies and gaining cross-cultural exposure adds value, supports career growth and helps reduce employee turnover. Hands-on learning through real-world challenges and emerging technologies can foster a culture of innovation—especially among Gen Zs in the industry.

GCCs in India have a mammoth task to attract and retain talent, given that demand for skilled professionals is expected to surpass supply in the coming years. Today, it is essential to constantly upgrade workplace policies to keep pace with the changing needs. With the right focus on innovation, inclusivity and employee development, GCCs are well-positioned to become global talent hubs that not only meet but shape the future of work.

-

GCCs Favour India’s Non-Core Business Districts, Boosting Office Market

India’s Global Capability Centres (GCCs) are increasingly favouring secondary and peripheral business districts (SBDs and PBDs) in major cities, according to a recent report by Realty+. These areas, which are often located near employee catchment areas and have seen significant improvements in accessibility due to infrastructure developments, are becoming attractive locations for GCCs.

The report highlights that over the past five years, nearly 70 million sq ft of GCC demand has been concentrated in the top 10 micro markets in India, accounting for 73% of the total GCC leasing in the country.

Micro markets such as Bengaluru’s Outer Ring Road (ORR) and Whitefield, Hyderabad’s Secondary Business District (SBD) and Off SBD, and Chennai’s Old Mahabalipuram Road (OMR) Zone 1 and Muttukadu-Pradeshivakkam Road (MPR) have collectively accounted for two-thirds of the country’s Grade A space uptake by GCCs since 2020.

According to the report, GCCs in India are spread across micro markets with a wide rental spectrum and continue to favour the country due to the availability of skilled talent, sectoral diversification, and usage functionality of GCC hubs.

“Global companies will continue to prefer having a presence in SBDs & PBDs of major Indian cities which are nearer to the employee catchment areas and have seen significant improvements in accessibility driven by infrastructure developments,” the report states.

The high-activity micro markets, which are spread across SBDs and PBDs, have accounted for two-thirds of India’s Grade A office demand and supply since 2020. These micro markets are expected to continue driving the office market in India over the next few years, with each of them likely to witness at least 1 million sq ft of average annual demand and supply.

The report also points out the importance of emerging micro markets, which are expected to witness considerable traction and increasingly complement the larger micro markets. As the GCC sector continues to play a significant role in driving India’s office market, SBDs and PBDs are emerging as key locations for these centres.

The growth of GCCs in India is driven by the country’s large pool of skilled talent, favourable business environment, and government initiatives to support the sector. With the GCC sector expected to continue growing, India’s office market is likely to see significant demand for high-quality office space in the coming years.

The report suggests that GCCs will remain a key driver of India’s office market, with SBDs and PBDs emerging as preferred locations for these centers. As the sector continues to evolve, it will be interesting to see how the office market in India responds to the growing demand for high-quality office space.